The CAS Annual Meeting Through the Eyes of Trust Scholarship Recipients

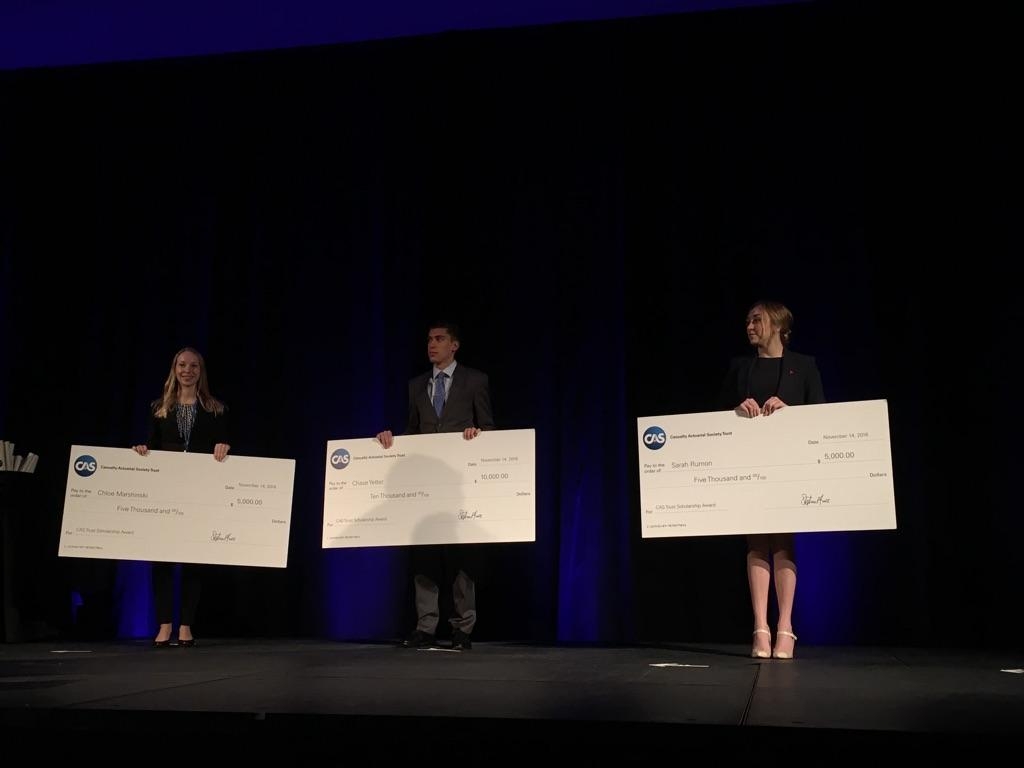

One of the perks of being a CAS Trust Scholarship winner is getting to attend the CAS Annual Meeting, most recently held this November in Orlando, Florida. While the meeting is designed for property and casualty actuaries to learn about latest happenings in the actuarial field, earn continuing education credits, and network with peers and colleagues, what is it like to attend the meeting as an actuarial college student? Well we asked this year’s CAS Trust Scholarship recipients, $10,000 award winner, Chase Yetter of Lebanon Valley College, and $5,000 award winners, Chloe Marshinski of University of Illinois at Urbana-Champaign and Sarah Rumon of University of St. Thomas, to share insights from their experience.

Favorite Sessions or Presentations

Chase Yetter:

“THE UNDERWRITING CYCLE — IS IT ECONOMICS OR BEHAVIOR OR BOTH?” was my favorite session. We were able to hear from insurance executives on their thoughts regarding the predictability of the underwriting cycle, or lack thereof. I find this to be a really interesting topic and I always appreciate the opportunity to hear from industry leaders.

Chloe Marshinski:

I really enjoyed the keynote speaker, Simon Bailey. He was funny and engaging and it was interesting to hear about someone’s experiences in a field very different from actuarial. I also attended the break-out session on the new Predictive Analytics credential, which was very helpful for me as that is something I may consider pursuing in the future.

Sarah Rumon:

One of my favorite sessions was the general session that addressed the underwriting cycle and debated whether it is an economic phenomenon or simply a behavioral cycle. For those who are only beginning their actuarial careers, I have found that there is not always much emphasis on how business functions (such as underwriting) impact actuarial functions and vice versa, so this was a refreshing perspective. I also enjoyed the keynote speaker Simon T. Bailey, who spoke about leadership and influencing team members to achieve goals that ultimately benefit the entire organization.

Networking with CAS Members

Chase:

I really enjoyed meeting members of the CAS and learning about their careers as well as the opportunities that are available to actuaries. They were very welcoming and provided great advice for students entering the field.

Chloe:

I really enjoyed meeting the CAS members during the meals and breaks. At breakfast and lunch, I sat with people from all different companies, and it was interesting to hear about all their experiences with the exam process and working as full time actuaries.

Sarah:

At the CAS meeting, there was such a wide variety of members—from actuaries that had just completed their ACAS, to chief actuaries who have been in the profession for years. It was incredibly motivating and encouraging to meet and network with so many actuaries who have each had unique career paths and experiences. There is something to learn from everyone!

Best Thing about the Annual Meeting

Chase:

Attending CAS meetings has shown me, through the wide variety of continuing education offered, that the CAS is ready to adapt to changes in the P&C profession. I’m excited to follow the development of new educational opportunities from iCAS.

Chloe:

The best parts of the meeting for me were the networking events. During both breakfast and lunch, I was able to reconnect with some of my coworkers at CNA as well as meet new people from other companies. I also enjoyed meeting and talking to the other two scholarship winners, Chase and Sarah…I am very excited to become a part of this community in the upcoming years and meet more people within the CAS.

Sarah:

By far, the highlight of the CAS Annual Meeting was the general excitement about the profession. All members were genuinely interested to learn from each other in a variety of sessions, and the ability to network with hundreds of actuaries was an amazing opportunity! Overall, I came away from the meeting more interested and excited to start a career in actuarial science.

The deadline for the 2017-2018 CAS Trust Scholarship is March 1, 2017. Additional information is available at casact.org/trustscholarship. Winners will be invited to attend the CAS Annual Meeting in Austin, TX in November 2017

In February we were happy to announce that CAS would be taking part in

In February we were happy to announce that CAS would be taking part in  Over the course of 2016 our CAS Student Central social media presence expanded and we wanted to use it to reach you directly and answer questions you might have, so we hosted our first

Over the course of 2016 our CAS Student Central social media presence expanded and we wanted to use it to reach you directly and answer questions you might have, so we hosted our first  In the fall, to help give you a broader look at the actuarial profession, we focused the CAS Student Central webinar on

In the fall, to help give you a broader look at the actuarial profession, we focused the CAS Student Central webinar on

Compensation – What are they offering financially? The base salaries offered by both companies may be similar, but you must also consider a few other factors. Look at bonus potential (are you even eligible?), student program bonuses and raises for passing exams and receiving credentials, and company benefits. What might seem like a similar pair of salaries may seem very different when you dive into the details.

Compensation – What are they offering financially? The base salaries offered by both companies may be similar, but you must also consider a few other factors. Look at bonus potential (are you even eligible?), student program bonuses and raises for passing exams and receiving credentials, and company benefits. What might seem like a similar pair of salaries may seem very different when you dive into the details. Career Path – Is there room at your potential employer for growth? Will you be part of a rotational program or will you be slotted into a role for the foreseeable future? Consider the size of the company and how actuaries move along their career path. If the company is small you might not have the opportunity to move up. If the company is large, you may be doing a very narrowly defined job that will not give you the skills to move forward.

Career Path – Is there room at your potential employer for growth? Will you be part of a rotational program or will you be slotted into a role for the foreseeable future? Consider the size of the company and how actuaries move along their career path. If the company is small you might not have the opportunity to move up. If the company is large, you may be doing a very narrowly defined job that will not give you the skills to move forward. Companionship – Did you like the people you met on your interview? You will be spending a very large portion of your waking hours with your coworkers. If you don’t like them, or there just aren’t many of them, you might find yourself miserable or just plain lonely.

Companionship – Did you like the people you met on your interview? You will be spending a very large portion of your waking hours with your coworkers. If you don’t like them, or there just aren’t many of them, you might find yourself miserable or just plain lonely. Culture– Does the company culture fit your personality? If you are the laid back type, you might not be happy at a company that has a high speed, constantly changing landscape. Conversely, if you are a high-energy type-A personality, you might not enjoy working for a more conservative, slow paced organization. This is a good topic for questioning during the interview stage, so you can truly understand the company you are working for and how you would fit in terms of temperament.

Culture– Does the company culture fit your personality? If you are the laid back type, you might not be happy at a company that has a high speed, constantly changing landscape. Conversely, if you are a high-energy type-A personality, you might not enjoy working for a more conservative, slow paced organization. This is a good topic for questioning during the interview stage, so you can truly understand the company you are working for and how you would fit in terms of temperament.

The CAS has made it easier than ever to run an actuarial case competition for university students! With the help of practicing actuaries and some serious volunteer time, the CAS has developed two case competitions, complete with toolkits that offer you guidance and templates to run your own case competition.

The CAS has made it easier than ever to run an actuarial case competition for university students! With the help of practicing actuaries and some serious volunteer time, the CAS has developed two case competitions, complete with toolkits that offer you guidance and templates to run your own case competition.

Based on average survey ranking, the most risky Halloween monster is Dracula / Vampires. While no one selected Dracula as the most risky, almost all respondents ranked him (it?) second! Concerns about Dracula, from a risk management perspective, centered primarily around severity: if it bites you, that’s pretty much all she wrote, and you join the can’t-get-enough-of-that-O-positive club. Interestingly, the fact that Dracula is only active at night was used by respondents on both sides of the frequency issue, as an indication that the risk might be both lower and higher: active “only at night” versus “every night.” One person suggested that, from the standpoint of exposures, there’s only one Dracula – but don’t the bitten then also become vampires? Also, it was pointed out that the original Bram Stoker version could shapeshift, and was master of those he “recruited,” and thus had the potential to be a particularly grueling risk. These last few comments demonstrate the importance of correctly ascertaining and defining the essential characteristics of your risk, in order to properly quantify and assess the underlying exposure, as well as the frequency and severity potential.

Based on average survey ranking, the most risky Halloween monster is Dracula / Vampires. While no one selected Dracula as the most risky, almost all respondents ranked him (it?) second! Concerns about Dracula, from a risk management perspective, centered primarily around severity: if it bites you, that’s pretty much all she wrote, and you join the can’t-get-enough-of-that-O-positive club. Interestingly, the fact that Dracula is only active at night was used by respondents on both sides of the frequency issue, as an indication that the risk might be both lower and higher: active “only at night” versus “every night.” One person suggested that, from the standpoint of exposures, there’s only one Dracula – but don’t the bitten then also become vampires? Also, it was pointed out that the original Bram Stoker version could shapeshift, and was master of those he “recruited,” and thus had the potential to be a particularly grueling risk. These last few comments demonstrate the importance of correctly ascertaining and defining the essential characteristics of your risk, in order to properly quantify and assess the underlying exposure, as well as the frequency and severity potential. Here I must embarrassedly provide a caveat. When I first sent this survey to my colleagues, I had included only the first seven monsters – I had somehow forgotten zombies! Several recipients of the survey pointed out this dreadful lacuna (which I contend was caused by the insidiousness of zombies themselves, and their effect on my brain!), but by then it was too late to add zombies to the survey. Nevertheless, a few respondents themselves chose to add zombies to their rankings and, although the sample size is much smaller than for the other classes, zombies did achieve the second-highest risk ranking, very close behind Dracula / Vampires.

Here I must embarrassedly provide a caveat. When I first sent this survey to my colleagues, I had included only the first seven monsters – I had somehow forgotten zombies! Several recipients of the survey pointed out this dreadful lacuna (which I contend was caused by the insidiousness of zombies themselves, and their effect on my brain!), but by then it was too late to add zombies to the survey. Nevertheless, a few respondents themselves chose to add zombies to their rankings and, although the sample size is much smaller than for the other classes, zombies did achieve the second-highest risk ranking, very close behind Dracula / Vampires. This one surprised me a bit – clearly, I’m no horror expert. I thought that, for this dude, exposure would be low because he’s only a problem on nights with a full moon. But others felt that frequency per unit of exposure (on those infrequent nights, he has an insatiable appetite) and severity (if you happen to be in the same room with this guy, you’re probably dead) would be significant, even if the exposure itself is only about once per month.

This one surprised me a bit – clearly, I’m no horror expert. I thought that, for this dude, exposure would be low because he’s only a problem on nights with a full moon. But others felt that frequency per unit of exposure (on those infrequent nights, he has an insatiable appetite) and severity (if you happen to be in the same room with this guy, you’re probably dead) would be significant, even if the exposure itself is only about once per month. Coming in fourth on our list of greatest risk-hits are witches and wizards. A problem with them is quantifying the exposure level: you never quite know who is and isn’t a witch (who would have suspected Selena Gomez?!). And, like most of the high-risk-ranking monsters, the potential severity is enormous – one thought, or nose-wiggle, or finger-snap could take out the whole town. On the good side, with respect to frequency of damage, unless they’re provoked, they’re generally not harmful. So “just leave them alone” would be sound risk management advice!

Coming in fourth on our list of greatest risk-hits are witches and wizards. A problem with them is quantifying the exposure level: you never quite know who is and isn’t a witch (who would have suspected Selena Gomez?!). And, like most of the high-risk-ranking monsters, the potential severity is enormous – one thought, or nose-wiggle, or finger-snap could take out the whole town. On the good side, with respect to frequency of damage, unless they’re provoked, they’re generally not harmful. So “just leave them alone” would be sound risk management advice! There was some disagreement among respondents regarding The Mummy, and so here’s another example of the need to precisely identify, characterize, and define your risks. Some felt he should be low on the list (perhaps you can simply outrun him). Others were concerned that he’s the one on the list that truly seems to want to kill everyone, and that he himself can be hard to kill, requiring magic or an ancient Egyptian curse. (So I guess we can’t just nuke him?)

There was some disagreement among respondents regarding The Mummy, and so here’s another example of the need to precisely identify, characterize, and define your risks. Some felt he should be low on the list (perhaps you can simply outrun him). Others were concerned that he’s the one on the list that truly seems to want to kill everyone, and that he himself can be hard to kill, requiring magic or an ancient Egyptian curse. (So I guess we can’t just nuke him?) Now this is a really interesting one, and it has a very important lesson for actuaries and risk analysts. The responses and rankings on The Grim Reaper had by far the highest standard deviation of any of the eight monster types – i.e., there was more disagreement in the rankings. In fact, roughly the same number of people ranked TGR most risky, as ranked it least risky. I think what has happened here is a common issue: causality versus correlation. Let’s face it: if TGR shows up, you’re pretty much toast. But is TGR the cause of death, or just the messenger (and thus the link between TGR is one of correlation, rather than cause)? My interpretation (and again, we need to define and characterize our risks accurately!) is that death is caused by other factors, and TGR just shows up at the appropriate time. In that sense, TGR would not be risky per se – but would be a rather reliable indicator that death is imminent.

Now this is a really interesting one, and it has a very important lesson for actuaries and risk analysts. The responses and rankings on The Grim Reaper had by far the highest standard deviation of any of the eight monster types – i.e., there was more disagreement in the rankings. In fact, roughly the same number of people ranked TGR most risky, as ranked it least risky. I think what has happened here is a common issue: causality versus correlation. Let’s face it: if TGR shows up, you’re pretty much toast. But is TGR the cause of death, or just the messenger (and thus the link between TGR is one of correlation, rather than cause)? My interpretation (and again, we need to define and characterize our risks accurately!) is that death is caused by other factors, and TGR just shows up at the appropriate time. In that sense, TGR would not be risky per se – but would be a rather reliable indicator that death is imminent. Ghosts were generally low-rated, on the basis that they may be unable to do physical damage (although see Ghostbusters – “I think he can hear you, Ray”), and they tend to stick to their own stomping grounds. But there’s certainly potential for emotional distress and mental damage. Plus, again, how do we know the extent of the exposure?

Ghosts were generally low-rated, on the basis that they may be unable to do physical damage (although see Ghostbusters – “I think he can hear you, Ray”), and they tend to stick to their own stomping grounds. But there’s certainly potential for emotional distress and mental damage. Plus, again, how do we know the extent of the exposure? Not the brightest bulb on the tree, he can be both outrun and out-thought. (But what’s up with that haircut??)

Not the brightest bulb on the tree, he can be both outrun and out-thought. (But what’s up with that haircut??)

Last month,

Last month,  Health or medical insurance. This is a “first-party” insurance coverage, in which the policyholder’s own insurer responds with coverage for injury to the insured, regardless of whether or not a “third party” is liable. In our Pokémon hypothetical, medical expenses associated with your broken ankle, the car driver’s broken wrist, and the pedestrian’s dog bite would likely each be covered by that person’s own medical insurance.

Health or medical insurance. This is a “first-party” insurance coverage, in which the policyholder’s own insurer responds with coverage for injury to the insured, regardless of whether or not a “third party” is liable. In our Pokémon hypothetical, medical expenses associated with your broken ankle, the car driver’s broken wrist, and the pedestrian’s dog bite would likely each be covered by that person’s own medical insurance.

Auto insurance. Damage to the passing car, as well as any liability ascribed to the driver and/or owner of the passing car, would potentially be covered by an auto insurance policy.

Auto insurance. Damage to the passing car, as well as any liability ascribed to the driver and/or owner of the passing car, would potentially be covered by an auto insurance policy. covers the liability of the policyholder in two ways: coverage above the policy limits associated with the policyholder’s HO and auto policies, and “drop-down” or “gap” coverage for other types of liability not covered by HO and auto policies.

covers the liability of the policyholder in two ways: coverage above the policy limits associated with the policyholder’s HO and auto policies, and “drop-down” or “gap” coverage for other types of liability not covered by HO and auto policies.

This may be obvious to many, but your first barrier to entering the actuarial field will be completing at least one actuarial exam. Just about every full-time actuarial opportunity is going to require a minimum of one exam passed, and you will be even more marketable with 2-3 under your belt.

This may be obvious to many, but your first barrier to entering the actuarial field will be completing at least one actuarial exam. Just about every full-time actuarial opportunity is going to require a minimum of one exam passed, and you will be even more marketable with 2-3 under your belt. Regardless of being a current student, new college graduate, or career changer, actuarial internship experience will be a valuable addition to your background. I recognize that most internships are offered to current college students. However, on several occasions, I have worked with career changers who have been able to secure internships, even 10+ years out of college. While many internship descriptions may list “must be a current college student,” this is not always the case; it is still worth putting in an internship application, if you have the time, as you never know when a company may have flexibility. Keep in mind that most actuarial internships will also require at least one actuarial exam passed.

Regardless of being a current student, new college graduate, or career changer, actuarial internship experience will be a valuable addition to your background. I recognize that most internships are offered to current college students. However, on several occasions, I have worked with career changers who have been able to secure internships, even 10+ years out of college. While many internship descriptions may list “must be a current college student,” this is not always the case; it is still worth putting in an internship application, if you have the time, as you never know when a company may have flexibility. Keep in mind that most actuarial internships will also require at least one actuarial exam passed. Just about every actuarial job description that you review is going to include a combination of programming/computer skills. While Excel tends to be the number one utilized computer skill in the actuarial field, basic Excel skills are not really going to cut it anymore, if you want to be competitive. In addition to Excel, there tends to be quite a bit of demand for the following skills: Access, Visual Basic/VBA, SQL, SAS, C++, and R.

Just about every actuarial job description that you review is going to include a combination of programming/computer skills. While Excel tends to be the number one utilized computer skill in the actuarial field, basic Excel skills are not really going to cut it anymore, if you want to be competitive. In addition to Excel, there tends to be quite a bit of demand for the following skills: Access, Visual Basic/VBA, SQL, SAS, C++, and R. It is quite common for job seekers to write a cover letter template, switch out the company name and position title, and click “submit.” This is a missed opportunity to explain your specific interest in the company and role, and hiring teams may see this as a lack of effort and interest. Do some research, and explain why this company and position make sense for you, long term.

It is quite common for job seekers to write a cover letter template, switch out the company name and position title, and click “submit.” This is a missed opportunity to explain your specific interest in the company and role, and hiring teams may see this as a lack of effort and interest. Do some research, and explain why this company and position make sense for you, long term. One of the most common reasons that candidates do not move forward after an initial phone interview is that they did not appear to be knowledgeable about the company and position they are interviewing for. Make sure to thoroughly review the company’s website days before your interview, and print out a copy of the job description to have handy for your interviews. Take the time to draw parallels between your background (academics, work experience, technical skills, etc.), and the role you are applying to. It may also be helpful to write out a list that answers “Why am I interested in this specific company and role?” and also “Why am I a good fit?” Make sure to know the lines of business that the company works with.

One of the most common reasons that candidates do not move forward after an initial phone interview is that they did not appear to be knowledgeable about the company and position they are interviewing for. Make sure to thoroughly review the company’s website days before your interview, and print out a copy of the job description to have handy for your interviews. Take the time to draw parallels between your background (academics, work experience, technical skills, etc.), and the role you are applying to. It may also be helpful to write out a list that answers “Why am I interested in this specific company and role?” and also “Why am I a good fit?” Make sure to know the lines of business that the company works with. Adam Noreen is an Actuarial Recruiter at DW Simpson. He has been assisting entry-level candidates and career changers for approximately three years, in securing their first actuarial and analytics positions. Contact Adam at

Adam Noreen is an Actuarial Recruiter at DW Simpson. He has been assisting entry-level candidates and career changers for approximately three years, in securing their first actuarial and analytics positions. Contact Adam at

Suddenly, you see something, just ahead and to the left, on the periphery of your screen sensor. You instinctively shift your direction slightly, and slowly close in on the object. You switch to virtual camera mode — and there it is, standing over six-feet tall: a bi-pedal feline. Right in front of the window of a well-landscaped brick ranch home, just standing there like he owns the place. Not believing your luck, you blink and then refocus. Your eyes were not deceiving you. It is indeed one of the rarest (and strongest) of the Pokémon: Mewtwo. You simply must have it! But before you attempt the capture, you’d like to get much closer…

Suddenly, you see something, just ahead and to the left, on the periphery of your screen sensor. You instinctively shift your direction slightly, and slowly close in on the object. You switch to virtual camera mode — and there it is, standing over six-feet tall: a bi-pedal feline. Right in front of the window of a well-landscaped brick ranch home, just standing there like he owns the place. Not believing your luck, you blink and then refocus. Your eyes were not deceiving you. It is indeed one of the rarest (and strongest) of the Pokémon: Mewtwo. You simply must have it! But before you attempt the capture, you’d like to get much closer… You throw open the unlocked gate and step into the yard, breaking your ankle on a loose cobblestone. Undaunted, you limp purposefully toward the Mewtwo, trampling several expensive flowers and small ornamental shrubs. You fling your Pokéball, and score a direct hit – the Mewtwo is yours! In your ecstasy, you raise your arms in triumph, accidentally letting go of your phone, which flies into and shatters a window on the home.

You throw open the unlocked gate and step into the yard, breaking your ankle on a loose cobblestone. Undaunted, you limp purposefully toward the Mewtwo, trampling several expensive flowers and small ornamental shrubs. You fling your Pokéball, and score a direct hit – the Mewtwo is yours! In your ecstasy, you raise your arms in triumph, accidentally letting go of your phone, which flies into and shatters a window on the home. Chase Yetter, a rising senior at Lebanon Valley College double majoring in actuarial science and mathematics, was this year’s recipient of the $10,000 CAS Trust Scholarship. “When I was a student in high school, I knew I wanted to pursue a career that would challenge me, and I wanted it to involve both mathematics and business,” said Yetter. Chase is excited about a pursuing a career in the property and casualty industry, and has already been able to attend multiple industry events including the Spring 2015 and Fall 2015 Casualty Actuaries of the Mid-Atlantic Region (CAMAR) meetings, as well as the 2015 CAS Annual Meeting as part of the student program. “I hope to quickly become a Fellow of the Casualty Actuarial Society (FCAS) and a Chartered Property Casualty Underwriter (CPCU)… I also hope to become one of the first to earn the predictive analytics credential that arises from the partnership between the CAS and The Institutes.”

Chase Yetter, a rising senior at Lebanon Valley College double majoring in actuarial science and mathematics, was this year’s recipient of the $10,000 CAS Trust Scholarship. “When I was a student in high school, I knew I wanted to pursue a career that would challenge me, and I wanted it to involve both mathematics and business,” said Yetter. Chase is excited about a pursuing a career in the property and casualty industry, and has already been able to attend multiple industry events including the Spring 2015 and Fall 2015 Casualty Actuaries of the Mid-Atlantic Region (CAMAR) meetings, as well as the 2015 CAS Annual Meeting as part of the student program. “I hope to quickly become a Fellow of the Casualty Actuarial Society (FCAS) and a Chartered Property Casualty Underwriter (CPCU)… I also hope to become one of the first to earn the predictive analytics credential that arises from the partnership between the CAS and The Institutes.” Chloe Marshinski, a senior at the University of Illinois at Urbana-Champaign majoring in actuarial science and statistics, was awarded a $5,000 CAS Trust Scholarship. “Knowing my work is contributing to a field that helps our society function and grow gives me motivation and purpose in my work. I am specifically interested in the property-casualty industry because it encompasses so many different types of risk and is constantly faced with new challenges,” said Marshinski. She held an internship this past summer with CNA, where she completed two pricing reviews consisting of pulling and organizing data and making loss ratio selections, comprehensive pricing analysis of the umbrella book of business, and presented findings and recommendations on future business strategies to underwriting. Before that Marshinski interned with a State Farm agent, researching products, communicating with customers about their product interests, and calculating auto insurance quotes for online leads. Her internships taught her that “while the data and the numbers are important during an analysis, it’s being able to communicate your findings and recommendations to others that makes the analysis worthwhile.”

Chloe Marshinski, a senior at the University of Illinois at Urbana-Champaign majoring in actuarial science and statistics, was awarded a $5,000 CAS Trust Scholarship. “Knowing my work is contributing to a field that helps our society function and grow gives me motivation and purpose in my work. I am specifically interested in the property-casualty industry because it encompasses so many different types of risk and is constantly faced with new challenges,” said Marshinski. She held an internship this past summer with CNA, where she completed two pricing reviews consisting of pulling and organizing data and making loss ratio selections, comprehensive pricing analysis of the umbrella book of business, and presented findings and recommendations on future business strategies to underwriting. Before that Marshinski interned with a State Farm agent, researching products, communicating with customers about their product interests, and calculating auto insurance quotes for online leads. Her internships taught her that “while the data and the numbers are important during an analysis, it’s being able to communicate your findings and recommendations to others that makes the analysis worthwhile.” Sarah Rumon is an actuarial science major and rising junior at University of St. Thomas. She was awarded a $5,000 CAS Trust Scholarship. Rumon is the founding member and president of Gamma Iota Sigma Beta Pi Chapter at University of St. Thomas and was International Student Representative for Gamma Iota Sigma at the annual Gamma Iota Sigma Conference last year. Rumon has also taken part in the Travelers Insurance Actuarial Summer Student program as well as their Actuarial and Analytics Leadership Development Programs, where she summarized and presented aggregate review results to loss analytics department, and gained an understanding of public sector products. “During the course of my education and professional experiences thus far, I have come to realize that being an actuary is so much more than passing tough exams and being skilled with using Excel. To me, a successful actuary has three distinct sets of skills: analytical skills, business acumen and knowledge, and soft skills such as leadership, communication, time management, and more,” said Rumon.

Sarah Rumon is an actuarial science major and rising junior at University of St. Thomas. She was awarded a $5,000 CAS Trust Scholarship. Rumon is the founding member and president of Gamma Iota Sigma Beta Pi Chapter at University of St. Thomas and was International Student Representative for Gamma Iota Sigma at the annual Gamma Iota Sigma Conference last year. Rumon has also taken part in the Travelers Insurance Actuarial Summer Student program as well as their Actuarial and Analytics Leadership Development Programs, where she summarized and presented aggregate review results to loss analytics department, and gained an understanding of public sector products. “During the course of my education and professional experiences thus far, I have come to realize that being an actuary is so much more than passing tough exams and being skilled with using Excel. To me, a successful actuary has three distinct sets of skills: analytical skills, business acumen and knowledge, and soft skills such as leadership, communication, time management, and more,” said Rumon.